The Inflation Reduction Act, was recently passed. One of the major points in this legislations is that it will make it easier for nonprofit organizations to go solar. This legislation allows nonprofit organizations to take advantage of the same solar tax credits that are available to businesses, making it more financially viable for them to switch to clean, renewable energy.

One of the main barriers that has prevented many nonprofits from going solar in the past is the upfront cost of installation. Solar panel systems can be expensive to install, and many nonprofit organizations simply don’t have the budget for it. The Solar for Nonprofits Act addresses this issue by allowing nonprofits to claim the solar investment tax credit (ITC), which can significantly reduce the cost of going solar.

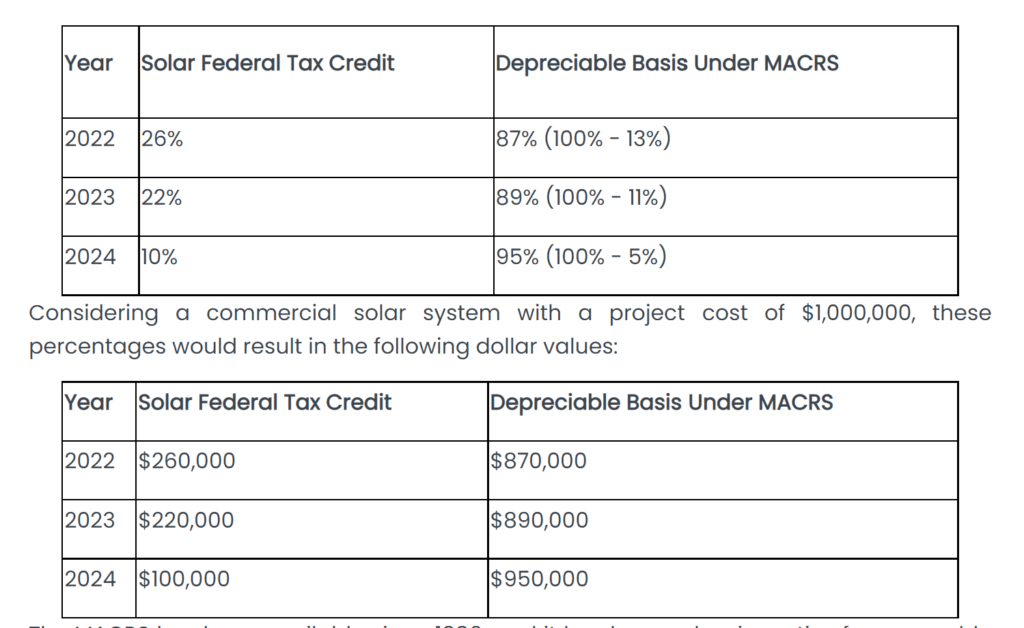

The ITC allows organizations to claim a credit worth up to 26% of the cost of their solar panel system. This can make a significant difference in the affordability of going solar, and it’s a game changer for many nonprofit organizations that may have previously been unable to afford the upfront cost.

In addition to the ITC, the Inflation Reduction Act also includes other provisions that will help make it easier for nonprofits to go solar. For example, it allows organizations to claim the credit even if they don’t have a tax liability, which is a common issue for nonprofit organizations. This means that they can still claim the credit and use it to offset the cost of their solar panel system, even if they don’t owe any taxes.

Renewable energy is becoming a key priority for many lenders. To support the UN’s Sustainable Development Goals of affordable and clean energy, sustainable cities and communities, climate action and partnerships, many banks are developing specialized commercial loan products designed to encourage the use of solar energy. These loan products include loans for rooftop solar systems, loans for energy efficiency improvements, sustainably certified commercial real estate financing, and sustainably certified construction loans.

Banks focused on accelerating the transition to clean energy are best positioned to help nonprofits secure advantageous funding for their solar installations. There are specialist lenders that have the institutional knowledge and technical know-how to develop innovative funding structures with favorable rates and terms designed to help nonprofits finance these installations.

There is no doubt that the IRA coupled with financing tools that provide funding support for clean energy projects will catalyze nonprofit organizations to deploy solar energy and speed their transition to a net-zero emissions future. Going solar will offer these organizations long-term cost savings while providing the benefits of combatting climate change, creating jobs and bringing new investment into their communities.

Summing up the bottom-line benefits of the IRA, a blog post by Candace Vahlsing, associate director for climate, energy, environment, and science with the White Houses’ Office of Management and Budget, said “the Inflation Reduction Act will help ease the burden that climate change imposes on the American public, strengthen our economy, and reduce future financial risks to the Federal Government and to taxpayers.”

Overall, the Inflation Reduction Act is a major win for nonprofit organizations that are looking to switch to clean, renewable energy. It removes many of the financial barriers that have previously made it difficult for these organizations to go solar, and it makes it more financially viable for them to make the switch. As a result, we can expect to see more and more nonprofit organizations going solar in the coming years, which is great news for the environment and for the future of renewable energy.